The Polish Financial Supervision Authority (KNF) is one of the most important regulatory bodies in Poland’s financial sector. Whether you are opening a bank account, purchasing insurance, investing in stocks, or trading forex, the KNF plays a critical role in ensuring that financial institutions operate fairly and transparently.

For investors and traders, understanding how the KNF works can help you identify legitimate financial firms, avoid scams, and make more informed decisions. This guide explores the authority’s responsibilities, regulatory powers, licensing procedures, and its impact on Poland’s financial markets.

Click Here To Join our Telegram Community

What Is the Polish Financial Supervision Authority (KNF)?

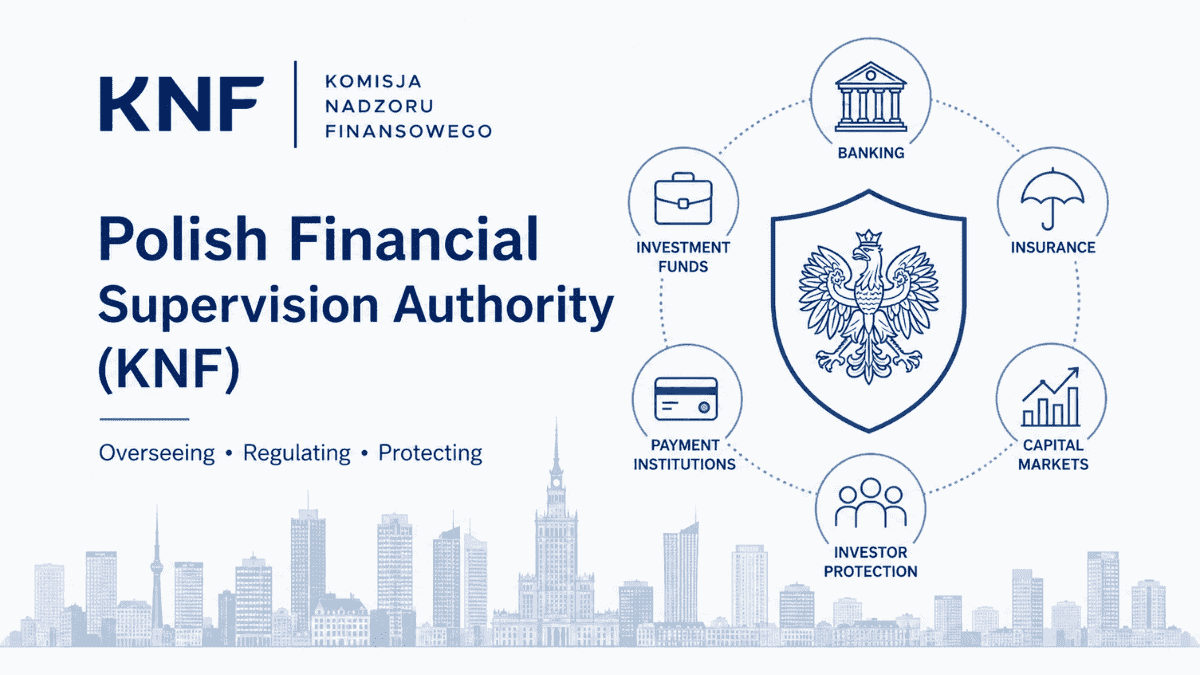

The Polish Financial Supervision Authority, known by its Polish acronym KNF (Komisja Nadzoru Finansowego), is the primary financial regulator in Poland.

Its main responsibility is to oversee the country’s financial system and ensure that regulated institutions comply with applicable laws and regulations. The authority was established to strengthen financial stability, improve market transparency, and protect consumers from unfair practices.

Unlike regulators that focus on a single sector, the KNF supervises multiple areas of the financial industry. This integrated approach allows it to monitor risks across the broader financial ecosystem rather than treating each sector independently.

Why Was the KNF Created?

Understanding the regulator’s origins helps explain its current responsibilities.

The KNF was established in 2006 as part of Poland’s effort to modernize and strengthen financial oversight. Before its creation, different financial sectors were regulated by separate supervisory bodies.

The government recognized that modern financial institutions often operate across multiple sectors. A bank may offer investment products, insurance services, and payment solutions simultaneously. Consolidating supervision under one authority improved coordination and risk management.

The result was a more unified regulatory framework capable of responding to increasingly complex financial markets.

The Main Objectives of the KNF

The KNF’s mission extends beyond enforcing regulations. Its broader goal is to maintain trust in Poland’s financial system.

The authority focuses on several key objectives:

- Protecting consumers and investors

- Ensuring financial market stability

- Promoting transparency and fair competition

- Supervising regulated financial institutions

- Preventing market abuse and financial misconduct

- Supporting the long-term development of the financial sector

These objectives help create an environment where businesses can operate efficiently while consumers receive appropriate protection.

Which Financial Sectors Does the KNF Regulate?

The KNF oversees a wide range of financial institutions and activities.

Banking Sector

Banks are among the most heavily regulated institutions in Poland. The KNF monitors capital adequacy, liquidity, risk management practices, and compliance with banking laws.

Regular supervision helps ensure that banks remain financially sound and capable of meeting their obligations to customers.

Insurance Companies

Insurance providers must maintain sufficient reserves and comply with strict operational requirements.

The KNF supervises insurers to ensure they can pay claims, manage risks appropriately, and treat policyholders fairly.

Capital Markets

The authority oversees stock exchanges, brokerage firms, investment companies, and market participants.

Its responsibilities include monitoring trading activity, preventing market manipulation, and ensuring transparency in securities markets.

Investment Funds

Investment funds that manage client assets are subject to KNF supervision.

The regulator ensures that fund managers operate in accordance with applicable regulations and disclose risks properly to investors.

Pension Funds

Retirement savings are critical to long-term financial security.

The KNF supervises pension funds to help protect contributors and maintain confidence in the retirement system.

Payment Institutions

The growth of digital finance has expanded the regulator’s responsibilities.

Payment service providers, electronic money institutions, and certain fintech companies fall under KNF oversight, depending on the nature of their activities.

How the KNF Protects Investors

Investor protection is one of the most visible aspects of the KNF’s work.

Financial markets naturally involve risk. However, investors should not have to worry about fraud, misleading information, or unlawful business practices. The KNF works to reduce these risks through supervision, enforcement, and education.

The authority reviews disclosures made by regulated entities and investigates suspicious activities when necessary. It also issues warnings about unauthorized firms that may be operating illegally.

For example, if a company offers investment services without the required authorization, the KNF can place it on the warning lists and take enforcement action.

This helps investors identify potential threats before committing their money.

KNF and Forex Brokers

Forex traders frequently encounter references to the KNF regulation when evaluating brokers.

Any forex broker seeking to provide regulated investment services in Poland must meet strict regulatory requirements. These requirements often include minimum capital standards, internal compliance systems, risk management procedures, and client fund protection measures.

A KNF-regulated broker is generally required to:

- Segregate client funds from company funds

- Maintain adequate capital reserves

- Provide transparent pricing and disclosures

- Implement anti-money laundering controls

- Submit to ongoing regulatory supervision

While regulation cannot eliminate trading risk, it can reduce the likelihood of misconduct and operational failures.

The Licensing Process Under the KNF

Obtaining a KNF license is a rigorous process designed to ensure that only qualified firms enter the market.

Application Review

Companies must submit detailed documentation regarding their ownership structure, management team, business model, and financial resources.

Regulators carefully examine these materials to determine whether the applicant meets regulatory standards.

Capital Requirements

Many regulated financial activities require firms to maintain minimum capital levels.

Capital serves as a financial buffer that helps institutions absorb losses and continue operating during difficult market conditions.

Governance Assessment

The KNF evaluates the suitability of company directors and key managers.

Executives must demonstrate the necessary experience, qualifications, and integrity to manage regulated financial institutions responsibly.

Ongoing Supervision

Receiving a license is only the beginning.

Licensed firms remain subject to continuous oversight, reporting obligations, inspections, and compliance reviews throughout their operations.

Enforcement Powers of the KNF

Regulation would be ineffective without meaningful enforcement mechanisms.

The KNF has the authority to investigate potential violations and impose sanctions when necessary. Depending on the severity of the misconduct, enforcement actions may include fines, restrictions on business activities, public warnings, or license revocation.

These powers help maintain discipline within the financial sector and discourage unethical behavior.

The possibility of regulatory action encourages firms to invest in compliance systems and internal controls.

KNF Warning Lists and Consumer Alerts

One of the most useful tools available to consumers is the KNF warning list.

The authority regularly publishes information about entities that may be conducting financial activities without proper authorization. This allows consumers to verify whether a company is operating within the regulatory framework.

Before opening an investment account or transferring funds to a financial provider, checking regulatory status can be a valuable precaution.

Many investment scams rely on convincing consumers that they are dealing with legitimate institutions. Public warning lists help expose these operations.

The KNF’s Role in Financial Stability

Financial supervision involves more than monitoring individual companies.

The KNF also contributes to the stability of Poland’s broader financial system. By assessing systemic risks, monitoring market trends, and coordinating with other regulatory bodies, the authority helps identify vulnerabilities before they become major problems.

This proactive approach became especially important following the global financial crisis, which demonstrated how problems at one institution can spread throughout the financial system.

Strong supervision helps reduce the likelihood of widespread disruptions.

Cooperation With European Regulatory Authorities

Poland’s financial system is closely connected to the wider European market.

As a result, the KNF works alongside various European supervisory bodies and international organizations. This cooperation supports consistent regulatory standards and facilitates cross-border supervision.

Financial firms increasingly operate across multiple countries. Collaboration between regulators helps address challenges that extend beyond national borders.

It also improves information sharing and strengthens investor protection throughout Europe.

Benefits of Choosing a KNF-Regulated Financial Institution

Many consumers specifically seek regulated firms because regulation offers important safeguards.

Some of the key benefits include:

- Greater transparency and accountability

- Regulatory oversight and supervision

- Stronger consumer protection mechanisms

- Higher compliance standards

- Enhanced trust and credibility

- Better dispute resolution processes

These benefits do not guarantee success or profitability, particularly in investments. They do, however, provide a more secure framework for financial transactions.

Challenges Facing the KNF

Like financial regulators worldwide, the KNF faces evolving challenges.

Growth of Fintech

Digital banking, cryptocurrency-related services, and innovative payment solutions continue to reshape financial markets.

Regulators must balance innovation with consumer protection while avoiding unnecessary barriers to technological development.

Cybersecurity Risks

Cyber threats have become a major concern for financial institutions.

The KNF increasingly focuses on operational resilience, cybersecurity preparedness, and incident response capabilities.

Cross-Border Financial Services

Many financial firms serve customers in multiple jurisdictions.

This creates additional supervisory complexity and requires close coordination with foreign regulators.

Emerging Investment Products

New financial products often develop faster than regulations.

The KNF must continually adapt its supervisory framework to address evolving risks while maintaining market integrity.

How to Verify Whether a Firm Is Regulated by the KNF

Checking a firm’s regulatory status should be part of every investor’s due diligence process.

Before opening an account or investing money, consider these steps:

- Visit the official KNF register.

- Verify the company’s legal name.

- Confirm its authorization status.

- Review any regulatory notices or warnings.

- Ensure the services offered match the firm’s authorized activities.

Taking a few minutes to verify a company’s credentials can help prevent costly mistakes.

KNF vs Other European Financial Regulators

Although the KNF shares many responsibilities with other European regulators, each authority operates within its national legal framework.

For example, regulators in different countries may have varying licensing procedures, enforcement approaches, and reporting requirements. Despite these differences, most European regulators pursue similar goals: investor protection, market integrity, and financial stability.

The KNF is widely regarded as a significant supervisory authority within Central and Eastern Europe due to the size and importance of Poland’s financial market.

The Future of the Polish Financial Supervision Authority

The financial sector continues to evolve rapidly, and the KNF’s role will likely expand alongside these changes.

Digital finance, artificial intelligence, cybersecurity, open banking, and new investment technologies are creating opportunities and risks that require ongoing supervision. Regulators must remain adaptable while preserving trust in the financial system.

The KNF’s ability to balance innovation with strong oversight will play a major role in shaping Poland’s financial future.

Final Thoughts

The Polish Financial Supervision Authority (KNF) serves as the cornerstone of financial regulation in Poland. Its oversight extends across banking, insurance, investment services, pension funds, and payment institutions, helping to maintain confidence in the country’s financial markets.

For consumers, investors, and traders, understanding the KNF’s role provides valuable insight into how financial institutions are regulated and monitored. Whether you are evaluating a forex broker, choosing an investment platform, or researching a financial company, verifying KNF regulation is an important step toward making safer, more informed financial decisions.

Frequently Asked Questions (FAQs)

What does KNF stand for?

KNF stands for Komisja Nadzoru Finansowego, which translates to the Polish Financial Supervision Authority. It is Poland’s primary financial regulatory body responsible for overseeing various sectors of the financial industry.

Is a KNF-regulated broker safe?

A KNF-regulated broker must comply with strict regulatory standards and be subject to ongoing supervision. While regulation cannot eliminate trading risks, it generally provides stronger protections than dealing with an unregulated broker.

Does the KNF regulate forex brokers?

Yes. Forex brokers offering regulated investment services in Poland may fall under KNF supervision. They must meet licensing, capital, compliance, and client protection requirements.

How can I check if a company is regulated by the KNF?

You can verify a firm’s regulatory status through official KNF registers and databases. Checking authorization before investing is a recommended due diligence practice.

Can the KNF shut down illegal financial operations?

The KNF has enforcement powers that allow it to investigate violations, issue warnings, impose sanctions, and take actions against unauthorized financial activities.

Does the KNF regulate cryptocurrency companies?

The regulatory treatment of cryptocurrency-related businesses depends on the services provided and the applicable legal framework. Certain activities may fall under KNF oversight, while others may be governed by separate regulations.

Why is the KNF regulation important for investors?

KNF regulation helps promote transparency, consumer protection, and market integrity. It provides oversight mechanisms designed to reduce misconduct and improve confidence in financial markets.

Trade Anytime, Anywhere with XM

Take your trading to the next level with a globally trusted forex and CFD broker. Enjoy competitive spreads, fast execution, and reliable customer support while trading securely.

With XM, you get access to powerful trading platforms, real-time charts, flexible account types, and advanced tools to help you analyze the markets and manage your trades efficiently. Start your journey today by opening a trading account for free and join millions of traders worldwide.

✅ Open an Account with XM